U.S. Equity Market Outlook: Q2 2025

.svg)

After a turbulent start to the year, we move into Q2 2025 with a cautious optimism, tempered by geopolitical shocks and fiscal volatility. President Trump’s escalating tariff regime has triggered severe retaliation from China, raising levies on U.S. goods to 125% and sowing uncertainty across global markets. Although major indices ended April 7th that week higher—driven by a midweek rebound following a surprise 90-day pause on reciprocal tariffs—volatility remains elevated, and investor sentiment remains fragile.

Beneath the chaos, however, the U.S. economy continues to show resilience. A strong labor market, robust corporate earnings, and long-term secular growth drivers—AI, re-onshoring, and infrastructure modernization—support a base case of moderate expansion. Still, stagflation risks and recession probabilities are on the rise, requiring investors to remain flexible and defensively positioned.

The Macro Backdrop: Slower, Not Stalled

2024's 2.8% GDP growth was driven by pent-up demand and easing supply chains, but the foundations have weakened. New Fed guidance, combined with real-time business survey data, suggests U.S. GDP growth in 2025 may now fall below 2%, according to New York Fed President John Williams. Boston Fed President Susan Collins echoes the concern, warning that inflation could exceed 3.5% if tariffs persist.

The Trump administration's aggressive tariff hikes—now including a 145% levy on Chinese imports and 10–25% on others—have raised inflationary pressures across sectors. According to the University of Michigan’s April 2025 Consumer Sentiment Index, sentiment dropped to 50.8—its lowest reading since June 2022—reflecting growing pessimism around inflation and trade uncertainty. One-year inflation expectations surged to 6.7%, the highest level since 1981, as consumers braced for broader price increases across goods categories. This deterioration in confidence, paired with rising input costs, is beginning to erode corporate pricing power and could strain household balance sheets in the months ahead.

We maintain our forecast of two more Fed cuts in 2025, bringing the Fed Funds rate to 3.75–4.00% by early 2026. However, monetary easing alone won’t resolve the trade-driven disruptions. Without clearer fiscal and trade policies, business confidence and capital formation will remain subdued.

Earnings & Sentiment: The Corporate View is Changing

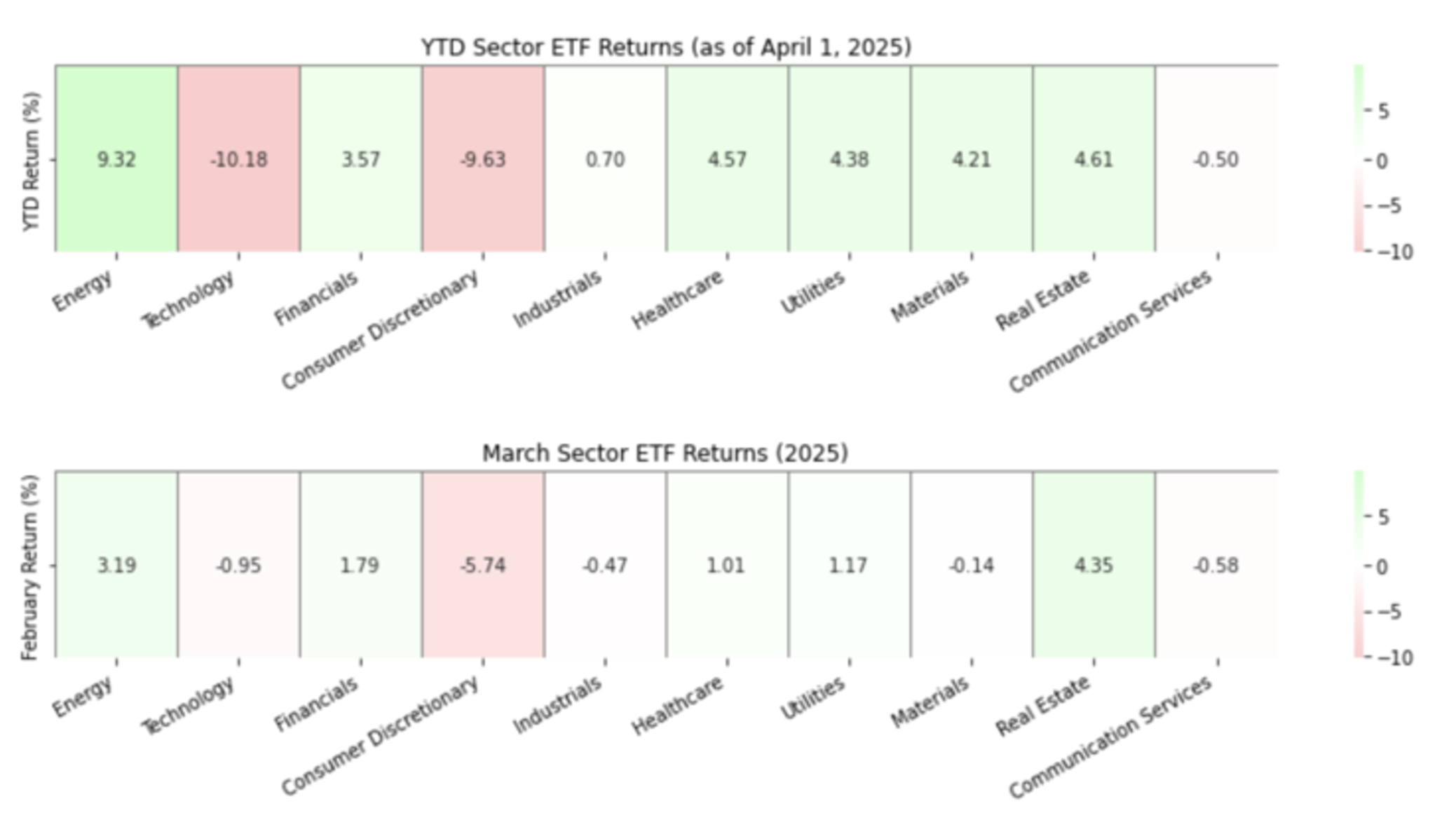

Q4 2024 earnings were strong and beat expectations broadly, fueling the S&P 500’s early-year rally. But sentiment has soured. The “Magnificent 7” tech names, which contributed over 70% of 2023–24 index gains, are now leading the pullback. As of late March, they have collectively declined ~20% from February highs, dragging the S&P 500 into negative territory for the year. Sector rotation is well underway, with defensive sectors—healthcare, staples, and utilities—outperforming amid the correction in growth.

Q1 earnings commentary has turned defensive. CEOs voiced concerns about tariff impacts, capital expenditure delays, and unpredictable regulatory environments. Despite this, underlying corporate fundamentals remain sound, supported by long-term tailwinds in digitization and AI. Consensus still calls for double-digit earnings growth through 2027, although near-term revisions are likely.

Investors should continue to view weakness in high-quality growth names—especially those with strong balance sheets and cash flow—as strategic entry points. In Q2, defensive sector rotation is not a sign of retreat but prudent recalibration.

Technology & AI: From Euphoria to Consolidation

The AI theme remains structurally intact but has entered a consolidation phase. The emergence of China’s DeepSeek-R1 model shook U.S. dominance in the space, raising questions about hyperscaler capex sustainability and AI profit trajectories. Yet, we view this disruption as part of a broader democratization of AI, where cheaper models enable wider adoption across sectors—finance, healthcare, industrials, and communications.

While the selloff in tech was necessary to deflate stretched valuations, we believe the sector remains central to future earnings growth. Names like AMZN, MSFT, and META continue to report strong top-line trends and retain cash-rich balance sheets, suggesting resilience despite sentiment-driven price corrections. Investors should treat weakness in high-quality AI and cloud players as strategic entry opportunities, not a signal of structural decline.

Trade Policy: Tariffs, Re-onshoring, and the Global Shuffle

Recent developments mark a sharp escalation in the global trade conflict:

- April 11: China retaliates by raising tariffs on U.S. goods from 84% to 125%, intensifying trade tensions and roiling markets.

- April 2–9: President Trump announces sweeping “reciprocal” tariffs, including a 145% levy on Chinese imports, triggering panic selling and historic intraday volatility.

- April 5: A universal 10% tariff is enacted on all non-USMCA imports, while non-compliant USMCA goods face 25% duties, except for energy and potash (10%).

The first two weeks of April have exposed the market’s acute sensitivity to tariff shocks. The rapid reinstatement and expansion of duties—particularly those affecting China and key commodities such as copper—are exacerbating cost pressures and destabilizing supply chains. U.S. firms, particularly in sectors reliant on foreign components like automobiles, electronics, and consumer durables, are experiencing mounting margin compression.

Still, there are structural tailwinds that could emerge. Re-onshoring momentum is likely to accelerate as companies look to sidestep unpredictable trade barriers. A steady rise in foreign direct investment into U.S. manufacturing is expected, which could strengthen domestic production capacity and benefit industrial REITs, logistics providers, and capital goods firms.

However, these realignments won’t come without geopolitical friction. As trade flows recalibrate, investors must pay closer attention to the shifting global alliances—especially the roles of Europe, India, and Southeast Asia, whose positioning in the U.S.–China power dynamic will increasingly shape global capital and supply chain flows.

Sector Strategy: Rotate, Rebalance, Reinforce

Against this backdrop of macro dislocation and earnings divergence, we are recalibrating our positioning to balance resilience with exposure to long-term innovation trends:

- Defensive Tilt with Selective Offense

Defensive sectors—healthcare, utilities, consumer staples—are gaining leadership in Q2. These areas offer earnings stability, strong dividend coverage, and lower exposure to tariff risk. However, we maintain exposure to growth sectors through select AI leaders, fintech innovators, and software-as-a-service companies with strong cash flow. - Quality and Dividends First

Amid macro noise, we favor companies with strong balance sheets, consistent free cash flow, and dividend growth. Blue-chip names across sectors—particularly in industrials and financials—can offer both capital preservation and upside through earnings surprises. - Thematic Tailwinds and Global Diversification

We’re overweighting global AI adopters, electrification infrastructure, and energy security plays. Internationally, we find compelling opportunities in Japan and India, where domestic demand, shareholder value creation, and innovation policy provide fertile ground. European equities, bolstered by fiscal stimulus and Ukraine ceasefire optimism, have begun to outperform and merit tactical allocation.

Risks to Watch in Q2

1. Stagflation Pressures Mounting

The combination of elevated inflation expectations and slowing growth is becoming harder to ignore. Fed officials now expect GDP growth below 1% for 2025, while inflation may breach 3.5–4%. If labor markets begin to weaken more visibly, the risk of stagflation—persistent inflation with stagnant growth—could materialize as a base-case scenario rather than a tail risk.

2. Tariff Shock Contagion

China's retaliatory move to raise tariffs on U.S. goods to 125%, alongside the U.S.'s 145% levy on Chinese imports, is hitting supply chains and input costs across industries. According to recent commentary on Q1 corporate earnings calls and supply chain analyst reports, industries such as automobiles, electronics, and consumer durables—which rely heavily on cross-border components—are already signaling elevated sourcing costs and logistical delays. While broader impacts may vary, continued policy uncertainty could delay investment decisions and weigh on manufacturing sentiment over the coming quarters.

3. Consumer Retrenchment Deepens

April consumer sentiment readings hit their lowest levels since mid-2022, with one-year inflation expectations jumping to 6.7%—the highest since 1981. If real wages erode and uncertainty persists, we could see a sustained pullback in discretionary spending, weakening the most important engine of U.S. GDP.

4. Corporate Margin Compression

Firms exposed to imported intermediate goods or global revenue streams are facing a margin squeeze, especially in autos, tech hardware, and consumer durables. As companies delay capex and shift production, profit forecasts for the second half of the year may be revised downward—potentially triggering earnings shocks and increased volatility.

5. Policy Gridlock and Global Realignment Risks

While the White House has introduced a 90-day pause on some tariffs, the underlying policy direction remains erratic. Budget clarity is lacking, tax reform is delayed, and allies remain wary. Any breakdown in U.S.–EU or U.S.–Asia diplomatic coordination could further fragment global trade alliances, reducing investor confidence and capital flows.

Conclusion: Prepare, Don’t Panic

The bull market is wounded, not dead. The first two weeks of April have been among the most volatile in recent memory, marked by sharp selloffs, dramatic rebounds, and a whiplash-inducing flow of trade policy headlines. Since April 2, markets have undergone painful recalibrations—but they have also demonstrated surprising resilience. While uncertainty remains elevated, we believe Q2 still offers a path toward stabilization—if not recovery—as earnings season progresses and tariff negotiations unfold. Investors should be prepared to remain agile and accept discomfort as part of the current investing landscape.

At Quantel Asset Management, we continue to believe in the transformative potential of AI, the resilience of the U.S. consumer, and the adaptability of corporate America. But we also recognize the deep structural shifts underway in global trade, fiscal policy, and investor sentiment. We remain focused on helping clients navigate this turbulence—balancing caution with opportunity and responding to a fast-changing world with strategic clarity, discipline, and adaptability.